Private blockchain infrastructure is moving from isolated proofs of concept into production-grade rails for banks, market infrastructure providers, and regulated financial networks. The reason is simple: public blockchains alone do not satisfy every banking requirement for privacy, identity, governance, deterministic execution, and controlled settlement.

For financial institutions, private blockchain infrastructure usually means permissioned DLT systems where participants are known, access is controlled, transaction visibility is governed, smart contracts execute predictable workflows, and audit records can be aligned with regulatory expectations.

This does not mean every bank should build its own blockchain. It means banks need to understand when private or permissioned DLT is the right architecture, how governance should work, which platforms fit which use cases, and what controls are required before production.

What Is Private Blockchain Infrastructure?

Private blockchain infrastructure is a permissioned distributed ledger environment where approved institutions, systems, or users participate under defined governance rules. Unlike open public networks, private DLT networks control who can join, which nodes can validate, what data each party can see, how upgrades are approved, and how disputes or exceptions are handled.

In banking, private blockchain infrastructure usually includes:

- Permissioned identity and access control.

- Node roles such as validators, participants, observers, notaries, or auditors.

- Privacy models for selective disclosure and private transactions.

- Deterministic smart contracts or workflow logic.

- Integration with custody, treasury, payments, compliance, and core systems.

- Governance rules for onboarding, upgrades, revocation, liability, and dispute resolution.

- Audit trails for initiations, approvals, signatures, state transitions, and settlement events.

The design goal is not decentralization for its own sake. The goal is shared infrastructure that can coordinate financial workflows across entities while preserving the controls that regulated institutions require.

Why Banks Are Moving from DLT Pilots to Production Rails

The first wave of banking DLT activity focused on exploration. Banks ran proofs of concept on Corda, Fabric, Quorum, and other platforms. Use cases included trade finance, KYC sharing, basic token models, and internal architecture experiments.

The second wave moved into structured pilots. Projects such as Jasper, Ubin, Helvetia, and Guardian tested interbank settlement, tokenized assets, and wholesale financial market infrastructure. Regulatory sandboxes in Europe, the UK, Singapore, and Hong Kong gave institutions more room to test tokenized settlement under supervision.

The current phase is production-oriented. Tokenized deposits, tokenized treasuries, money market funds, digital bonds, private DLT settlement rails, and cross-bank networks are moving from theory to controlled deployment. BIS Project Agora is a major example: the BIS Innovation Hub describes it as a project exploring tokenization of commercial bank deposits and central bank money on a programmable platform for cross-border payments, with multiple central banks and private-sector institutions involved. See the BIS overview of Project Agora.

Regulatory frameworks are also becoming more concrete. The EU DLT Pilot Regime, established under Regulation (EU) 2022/858, provides a framework for DLT-based market infrastructures such as DLT multilateral trading facilities, DLT settlement systems, and DLT trading and settlement systems. ESMA summarizes the regime and its scope on its DLT Pilot Regime page.

These signals point in the same direction: permissioned DLT is becoming part of the institutional infrastructure conversation, especially where privacy, governance, and settlement finality matter.

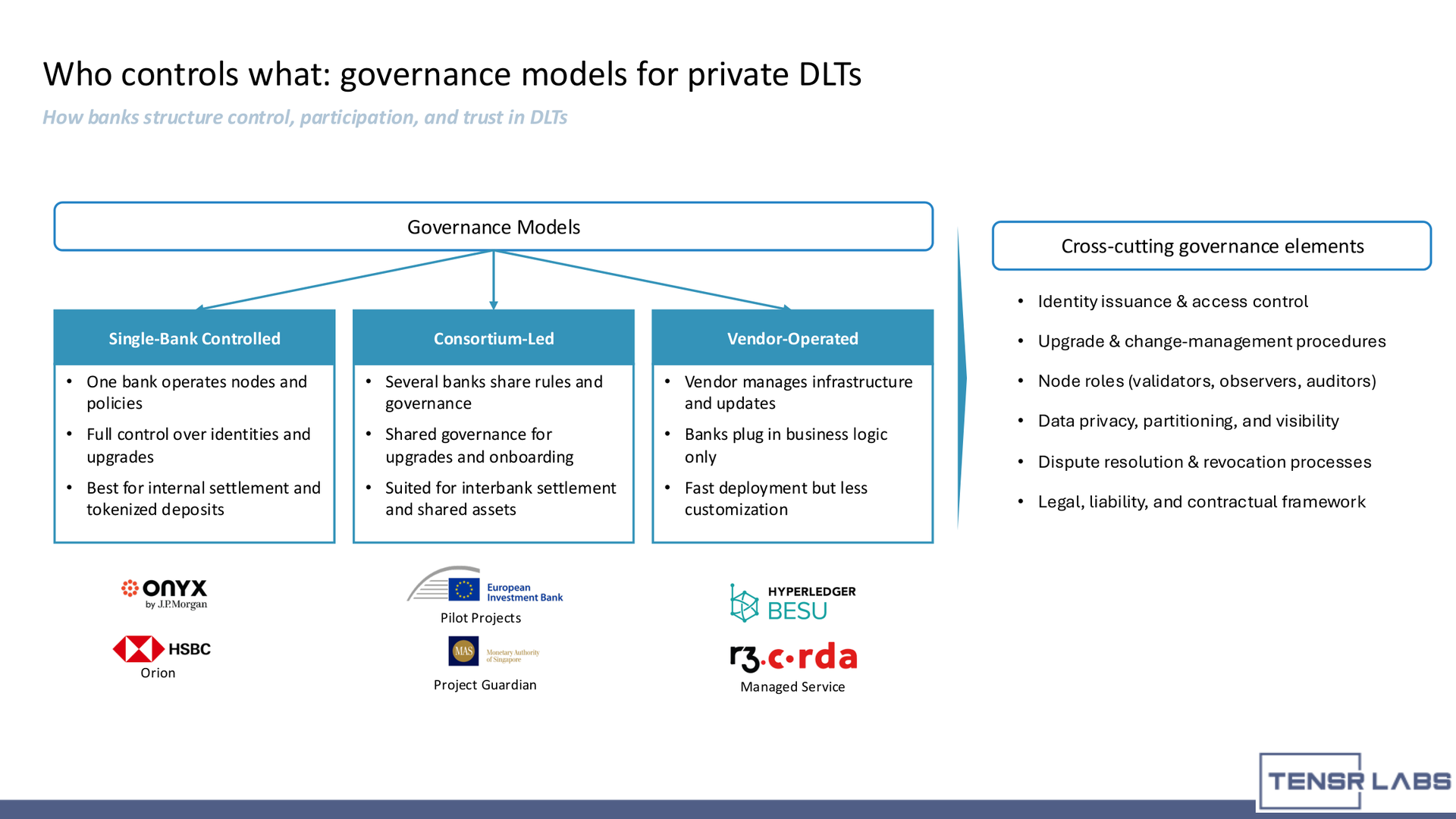

Governance Models: Single-Bank, Consortium-Led, and Vendor-Operated

The most important design decision in private DLT is not the chain itself. It is governance. Banks need to define who controls the network, who can participate, who can see data, who can upgrade contracts, who resolves disputes, and who is liable when something fails.

Single-Bank Controlled

In a single-bank model, one institution operates the nodes, rules, permissions, and upgrade process. This model is best suited for internal settlement, tokenized deposits, intragroup liquidity, treasury workflows, and bank-owned digital asset products.

The advantage is control. The bank can define identity, privacy, compliance, and integration requirements around its own operating model. The limitation is network reach. A single-bank network is less useful when the business case depends on many external counterparties.

Consortium-Led

In a consortium model, several banks or institutions share the network, rules, governance, onboarding, and upgrade procedures. This model is suited for interbank settlement, shared assets, collateral mobility, syndicated workflows, and market infrastructure use cases.

The advantage is shared adoption and network effects. The challenge is governance complexity. Participants need clear rules for membership, voting, upgrades, liabilities, data visibility, revocation, and operational responsibilities.

Vendor-Operated

In a vendor-operated model, a technology provider manages much of the infrastructure while banks plug in business logic, applications, or workflows. This can accelerate deployment and reduce internal operational burden.

The advantage is speed. The limitation is customization and control. Banks must understand what remains under their responsibility, what is delegated to the vendor, and how the arrangement satisfies audit, resilience, outsourcing, and regulatory expectations.

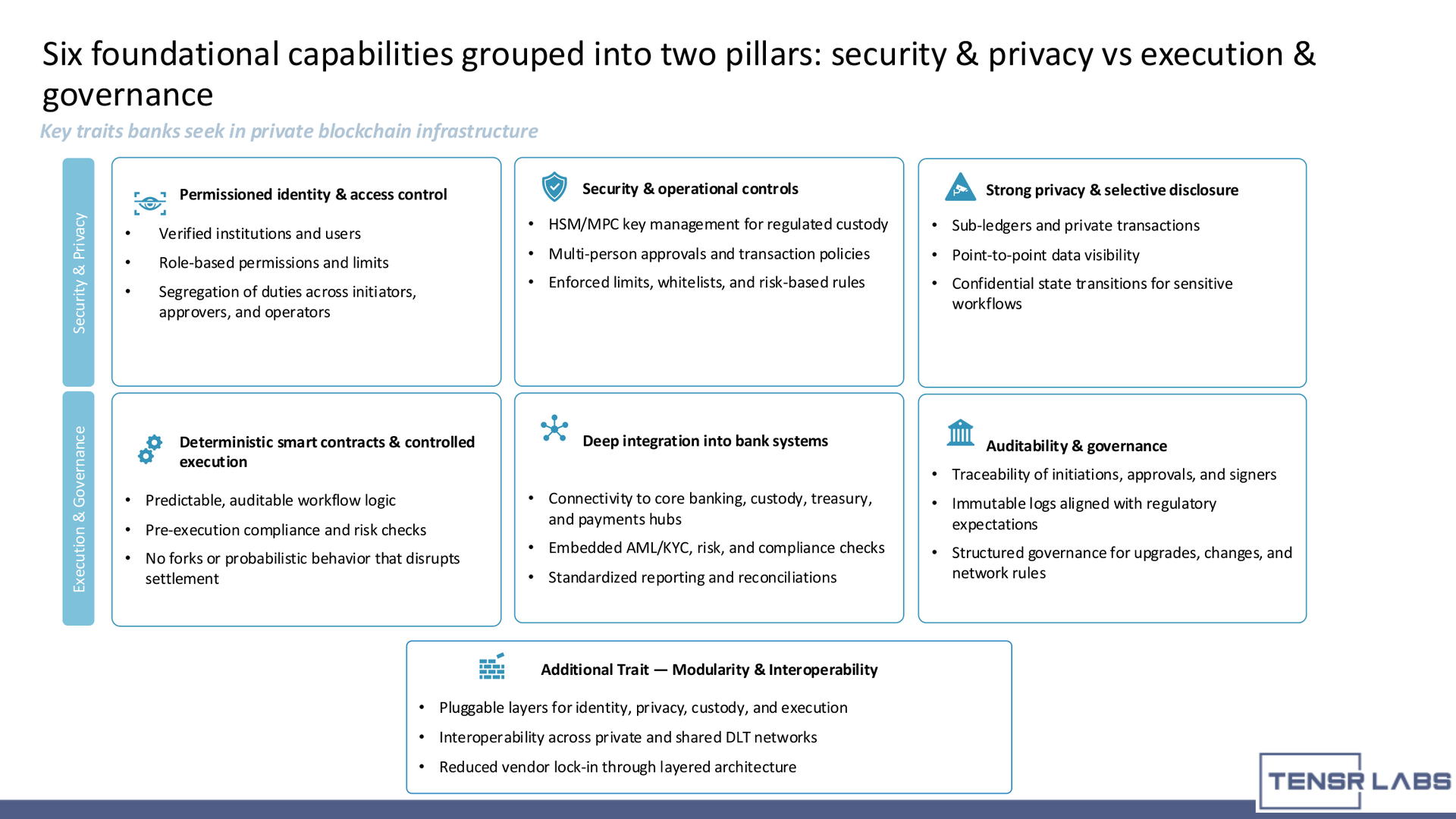

Six Capabilities Banks Need in Permissioned DLT

Private blockchain infrastructure should be evaluated against banking requirements, not only protocol features. Six capabilities matter most.

1. Permissioned Identity and Access Control

Every participant, node, user, and application should be tied to a verified identity. The network needs a mechanism for onboarding, revocation, role assignment, permissions, and segregation of duties.

This is the foundation for all other controls. If the network cannot explain who acted, under which role, and under which authority, it cannot serve regulated workflows.

2. Strong Privacy and Selective Disclosure

Banks cannot expose all transaction details to every participant. Private DLT networks must support selective disclosure, point-to-point visibility, confidential state transitions, sub-ledgers, or privacy domains depending on platform design.

Corda, for example, is explicitly designed around private transactions between relevant parties rather than global broadcast. R3 describes Corda as a private, permissioned DLT platform designed for financial services in its Corda documentation.

Canton takes a different approach, positioning itself as a privacy-enabled interoperable blockchain network for regulated financial institutions and institutional assets. Canton describes its model on the Canton Network protocol page.

3. Security and Operational Controls

Private DLT networks still require enterprise security. That includes HSM or MPC key management, multi-person approvals, transaction policies, whitelists, risk-based rules, node hardening, monitoring, and incident procedures.

The chain does not replace custody. It must integrate with custody and signing controls.

4. Deterministic Smart Contracts and Controlled Execution

Bank workflows need predictable execution. Settlement, collateral movement, tokenized deposit flows, and DvP processes cannot depend on unpredictable forks or uncontrolled state transitions.

Platforms address this differently. Corda uses flows and notarized state transitions. Hyperledger Besu can run private permissioned Ethereum networks with proof-of-authority consensus options such as IBFT 2.0 and QBFT. Hyperledger documents Besu as an Ethereum client for public and private networks, including permissioned network setup.

The key is not the label "smart contract." It is whether the execution model fits the bank's settlement, privacy, and audit requirements.

5. Auditability and Governance

Private DLT infrastructure must produce traceable records of initiations, approvals, signers, state transitions, exceptions, and final settlement. Auditability is a combination of on-ledger evidence, off-ledger approvals, custody signing logs, identity records, and governance documents.

The network should also define how rules change. Upgrades, node changes, participant onboarding, smart contract amendments, and revocations need formal governance.

6. Deep Integration Into Bank Systems

Private DLT cannot sit outside the institution's operating stack. It must connect to core banking, payments hubs, custody platforms, treasury systems, compliance tools, risk systems, reporting, and reconciliation workflows.

This integration layer is often where the most custom engineering is required. Platform selection matters, but production success depends on how well the DLT network fits into bank operations.

Privacy, Identity, and Selective Disclosure

Privacy is the main reason banks often choose private or permissioned DLT over public blockchain infrastructure. Financial institutions need to share enough data to settle and verify transactions, but not so much that sensitive customer, liquidity, pricing, or position data becomes visible to the wrong parties.

A bank-grade privacy model should define:

- Which parties can see transaction details.

- Which parties can validate state changes.

- Which observers or regulators can access audit views.

- Whether data is disclosed by transaction, asset, workflow, counterparty, or role.

- How confidential records are retained and retrieved.

- How privacy interacts with AML, dispute resolution, and reporting.

Identity and privacy must work together. A participant may need to prove eligibility without revealing unnecessary data. A regulator may need audit access without full operational control. A counterparty may need transaction assurance without seeing unrelated flows.

Private DLT platforms solve these problems differently. The right choice depends on whether the workflow is bilateral, consortium-based, asset-centric, EVM-compatible, or tied to broader financial-market infrastructure.

Execution, Smart Contracts, and Operational Controls

Private DLT networks are most valuable when they encode controlled financial workflows, not when they simply replicate a database. Useful workflows include tokenized deposit transfer, DvP settlement, collateral mobility, interbank netting, fund issuance, bond servicing, escrow, and conditional payments.

Execution logic should be:

- Deterministic.

- Auditable.

- Integrated with identity.

- Governed by pre-execution compliance checks.

- Protected by custody signing controls.

- Designed for exception handling.

- Connected to bank records after finality.

This is why private blockchain infrastructure is not only a protocol deployment. It is a full operating architecture. The DLT handles shared state and execution. The surrounding systems handle identity, approvals, custody, monitoring, compliance, reporting, and reconciliation.

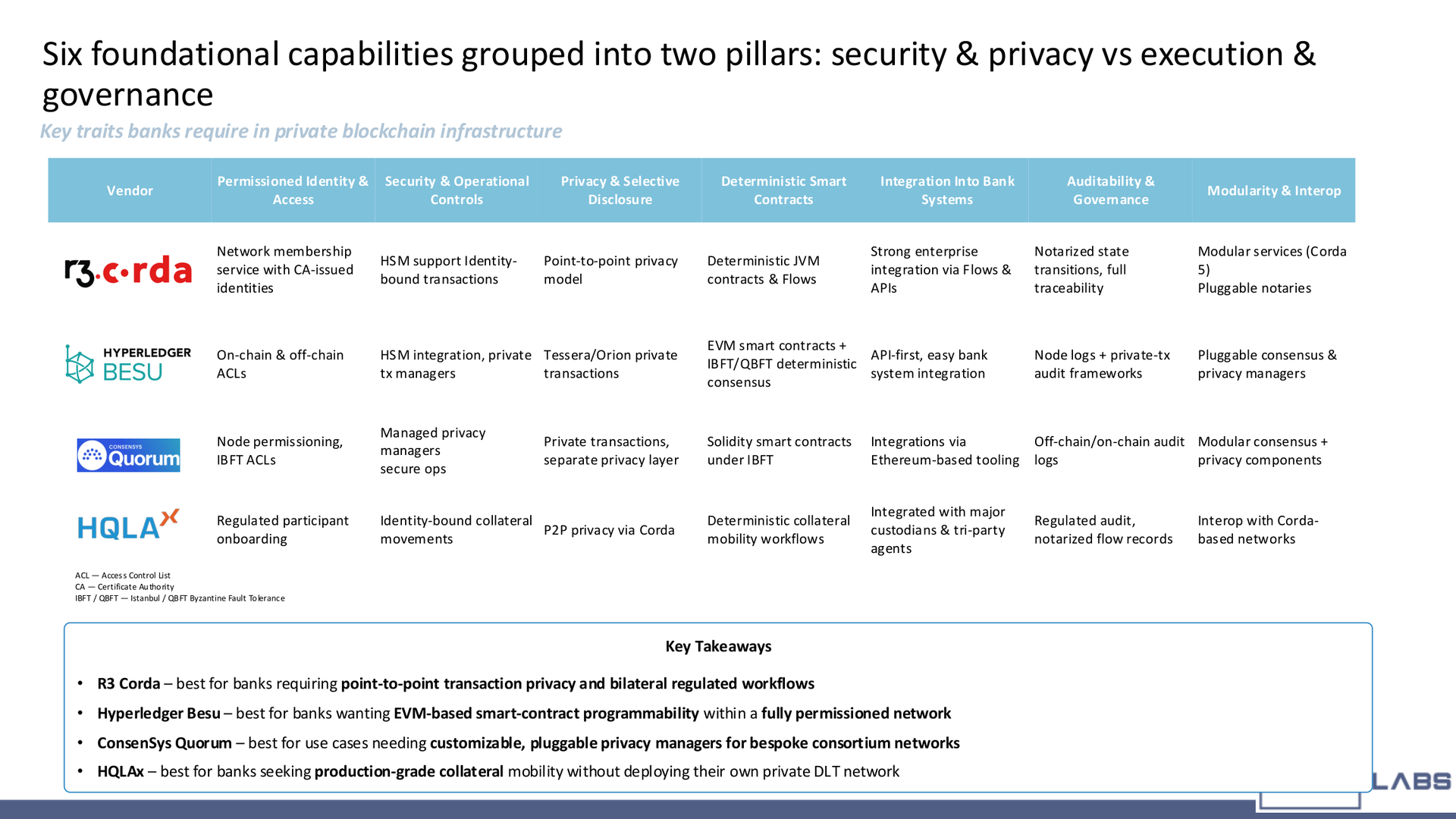

Platform Selection: Corda, Canton, Besu, Quorum, and Fabric

Banks should choose platforms based on workflow fit rather than generic rankings.

Corda

Corda is strong where financial institutions need point-to-point privacy, bilateral workflows, notarized state transitions, and enterprise financial services patterns. It is commonly considered for regulated settlement, syndicated workflows, trade finance, and private transaction models.

Canton

Canton is strong where institutions need privacy-preserving interoperability across applications and atomic workflows without exposing all data globally. It is relevant for regulated financial networks that need a "network of networks" model.

Hyperledger Besu

Besu is strong where banks want EVM-compatible smart contracts in a permissioned environment. It can fit tokenized deposits, RWA issuance, and private settlement workflows where Ethereum tooling and Solidity compatibility matter.

Quorum

Quorum and related permissioned Ethereum approaches can fit bespoke consortium networks that need EVM compatibility, private transactions, and customizable governance. Banks should evaluate the maturity of privacy tooling, throughput, support, and operational model.

Hyperledger Fabric

Fabric is strong for modular enterprise networks, identity-driven access, and consortium workflows. It is less asset-native than some alternatives, so token models and financial workflows may require more custom work.

The practical recommendation is to narrow the platform choice by use case:

- Use Corda or Canton when privacy and financial workflow design dominate.

- Use Besu or Quorum when EVM compatibility and smart contract portability matter.

- Use Fabric when modular enterprise identity and consortium architecture are priorities.

- Use managed or specialized networks when the business case is collateral mobility or market infrastructure access rather than deploying a bank-owned DLT.

How OQTACORE Can Help Design Private DLT Infrastructure

OQTACORE can help banks and market infrastructure teams design private blockchain infrastructure around the controls that matter in production.

At the first stage, OQTACORE can help evaluate Corda, Canton, Besu, Quorum, Fabric, and specialized private DLT networks against the institution's settlement, tokenization, privacy, governance, and integration requirements.

At the second stage, OQTACORE can design the permissioning architecture, identity model, node roles, privacy approach, smart contract workflow, custody integration, and audit trail for a specific use case.

At the enterprise stage, OQTACORE can act as the integration and orchestration partner across identity, access policies, smart contract workflows, custody connections, compliance engines, and audit data flows.

If your team is exploring internal settlement, interbank DLT, tokenized deposits, collateral mobility, or regulated RWA workflows, the right starting point is a private DLT architecture assessment. The goal is to decide not only which platform to use, but who controls what, who sees what, how transactions execute, and how the network fits into bank operations.

CTA: Discuss a private DLT architecture assessment with OQTACORE.

Presentation diagrams

The diagrams below are adapted from the source presentation and show the architecture, controls, and vendor landscape behind the article.

FAQ

What is private blockchain infrastructure?

Private blockchain infrastructure is a permissioned DLT environment where approved participants operate under defined rules for identity, access, privacy, validation, governance, smart contract execution, and auditability.

Why do banks use permissioned DLT instead of public blockchains?

Banks use permissioned DLT when they need known participants, selective disclosure, privacy, deterministic settlement, regulated governance, custom controls, and integration with internal systems. Public blockchains can still be useful, but they do not fit every banking workflow.

What governance models exist for private DLT networks?

The main models are single-bank controlled, consortium-led, and vendor-operated. Single-bank models maximize control, consortium models create shared networks, and vendor-operated models can accelerate deployment with less customization.

How do Corda, Canton, Besu, and Quorum differ?

Corda is strong for private financial workflows and point-to-point transaction privacy. Canton focuses on privacy-preserving interoperability across regulated applications. Besu supports EVM-compatible private permissioned networks. Quorum-style networks support permissioned Ethereum use cases with customizable privacy and governance.

What controls are required for private blockchain settlement?

Banks need permissioned identity, role-based access, privacy controls, custody integration, deterministic execution, compliance checks, approval workflows, audit logs, governance procedures, exception handling, and reconciliation with bank systems.

References

- BIS Innovation Hub, Project Agora

- BIS press release, Project Agora: central banks and banking sector embark on major project to explore tokenisation of cross-border payments

- ESMA, DLT Pilot Regime

- R3, Corda documentation

- Hyperledger Besu, permissioned network documentation

- Canton Network, protocol overview