Real-world asset tokenization is moving from experiment to infrastructure. Banks, asset managers, and issuers are no longer asking only whether assets can be represented on-chain. They are asking whether tokenized assets can be issued, governed, serviced, transferred, redeemed, and reported in a way that satisfies institutional operations and regulatory expectations.

A tokenization engine is the platform layer that makes this possible. It connects asset issuance, investor eligibility, smart contract logic, custody, compliance, lifecycle events, settlement, and reporting into one controlled operating model. For financial institutions, the token itself is only a small part of the system. The real value comes from the controls around it.

That distinction matters. A simple smart contract can mint a digital representation of an asset. A bank-grade tokenization engine has to bind that token to legal rights, investor rules, asset data, payment flows, custody controls, audit trails, and off-chain systems. Without that architecture, tokenization remains a pilot. With it, tokenization can become a production capability.

What Is a Tokenization Engine?

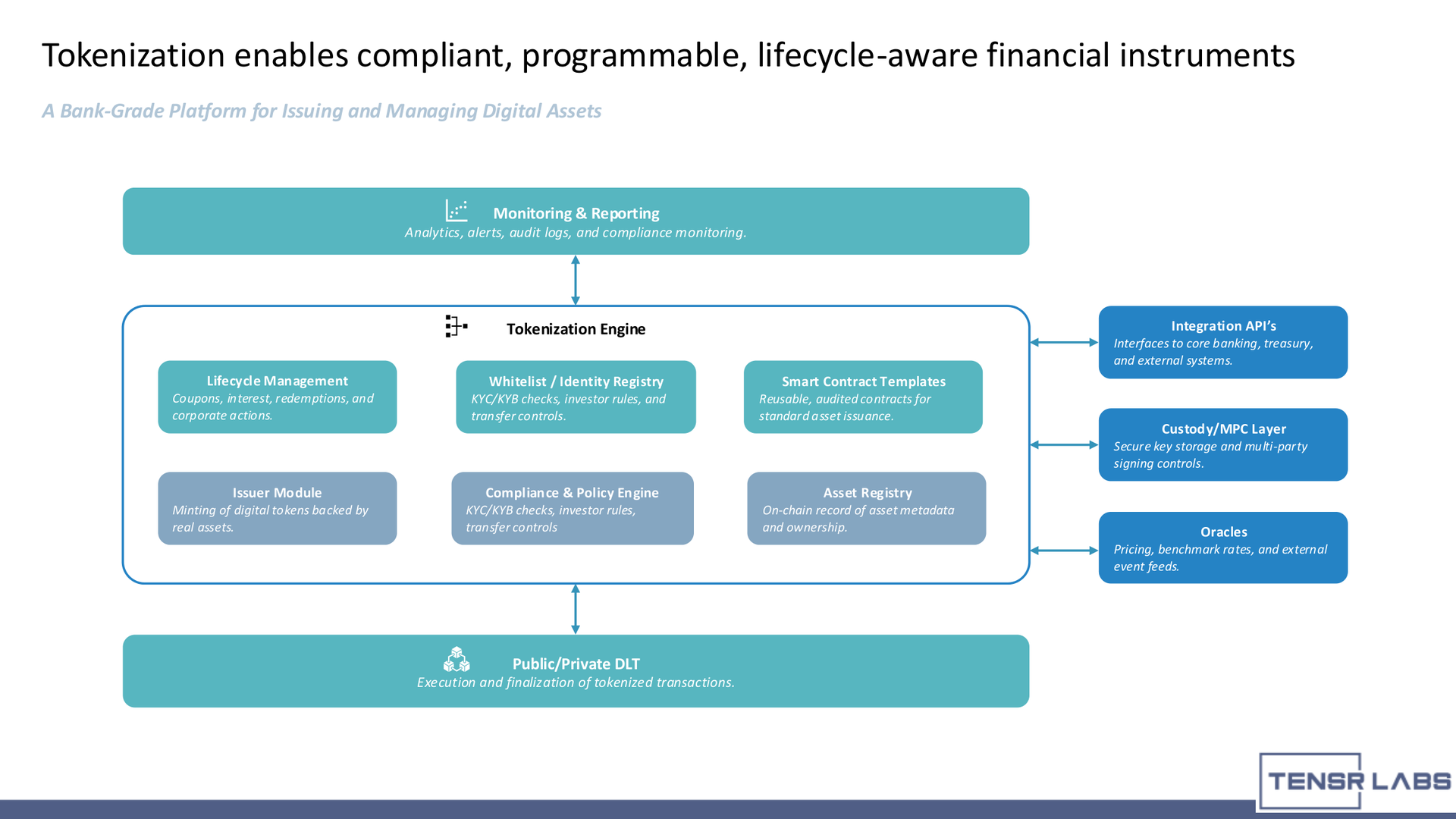

A tokenization engine is a software architecture for issuing and managing digital tokens that represent real-world assets. It typically includes an issuer module, asset registry, smart contract templates, compliance rules, investor whitelist, custody integration, lifecycle management, settlement workflows, monitoring, and reporting.

In practical terms, the tokenization engine sits between the traditional asset world and the blockchain execution layer. It translates real-world financial obligations into controlled on-chain actions:

- An issuer creates a tokenized asset.

- Eligible investors are onboarded and linked to approved wallets.

- Transfer rules define who can hold or move the token.

- Custody and signing controls protect issuance, movement, and redemption.

- Lifecycle events such as coupons, interest, maturities, redemptions, and corporate actions are executed and recorded.

- Monitoring and reporting systems produce the evidence needed by operations, auditors, and regulators.

This is why a tokenization engine should not be evaluated as a "minting tool" alone. In institutional settings, minting is the easy part. The harder work is enforcing the financial, legal, and compliance logic that makes the token usable in production.

Why Real-World Asset Tokenization Is Moving from Pilot to Production

Traditional asset infrastructure still carries several structural frictions. Asset lifecycle operations are often manual. Settlement can be slow. Liquidity is fragmented across systems, entities, custodians, and intermediaries. Compliance and audit data may sit in separate tools from the systems that execute transfers.

Tokenization addresses these problems by making assets programmable, traceable, and easier to move across controlled digital rails. That does not mean every asset should move on-chain immediately. It means institutions now have a technical path for redesigning workflows that previously depended on disconnected ledgers, spreadsheets, bilateral messages, and manual reconciliation.

The market signal is already visible. RWA.xyz tracks tokenized U.S. Treasuries as a multi-billion-dollar on-chain category, with products from issuers such as BlackRock, Franklin Templeton, Ondo, and others. See the RWA.xyz tokenized U.S. Treasuries dashboard. BlackRock's BUIDL fund and Franklin Templeton's BENJI / FOBXX fund show that regulated asset managers are not only experimenting with tokenization; they are operating live tokenized fund structures. CoinDesk reported BlackRock's BUIDL overtaking Franklin Templeton's tokenized treasury fund in 2024, and Franklin Templeton describes FOBXX as an on-chain U.S. government money fund. See CoinDesk's coverage of BlackRock BUIDL and Franklin Templeton's OnChain U.S. Government Money Fund.

Regulators and market authorities are also creating frameworks for controlled adoption. ESMA's DLT Pilot Regime provides a legal framework for DLT-based market infrastructures in the EU, including DLT multilateral trading facilities, DLT settlement systems, and DLT trading and settlement systems. The Monetary Authority of Singapore's Project Guardian has published fixed income and funds frameworks for tokenization use cases. See ESMA's DLT Pilot Regime and MAS Project Guardian.

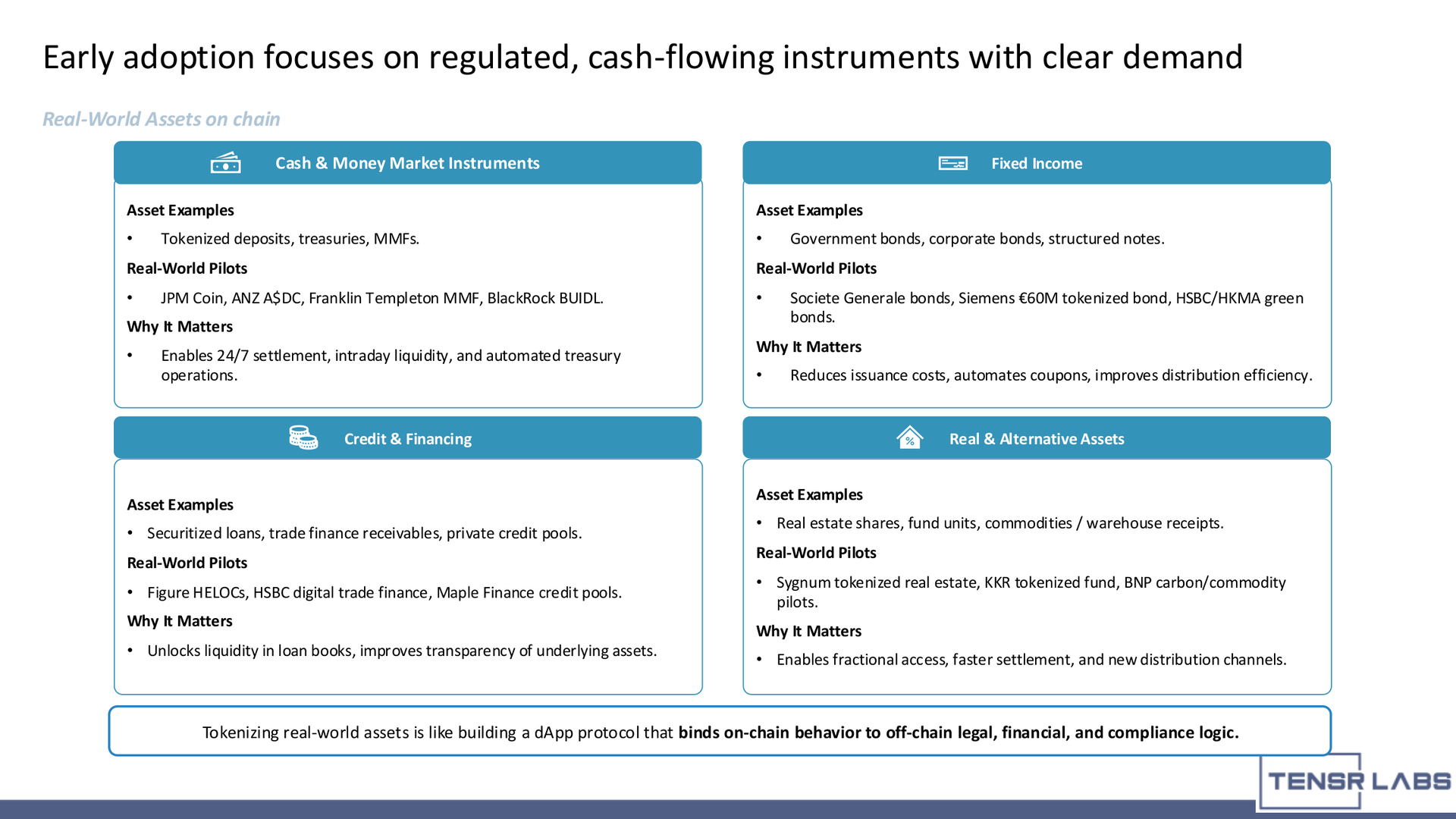

The clearest early opportunities are regulated, cash-flowing, or operationally complex instruments where better lifecycle automation and settlement visibility create tangible value. Examples include:

- Tokenized money market funds, treasuries, and deposits.

- Government and corporate bonds.

- Private credit pools, securitized loans, and trade finance receivables.

- Fund units, alternative assets, and real estate interests.

- Commodities or warehouse receipts where asset provenance and transfer restrictions matter.

The common thread is not that these assets are "crypto-friendly." It is that they have ownership records, eligibility rules, payment events, reporting requirements, and settlement needs. Those are exactly the workflows a tokenization engine is designed to coordinate.

Core Components of a Bank-Grade Tokenization Engine

A production tokenization engine needs more than a blockchain node and a set of smart contracts. For banks and asset managers, the platform usually includes several connected layers.

Issuer Module

The issuer module controls asset creation, issuance parameters, minting permissions, and redemption logic. It should support clear maker-checker workflows so that a single user cannot create, change, or issue assets without the required approvals.

For a tokenized bond, for example, the issuer module may define instrument metadata, maturity date, coupon logic, eligible holder classes, issuance cap, and redemption rules. For a tokenized fund unit, it may connect to fund administration, subscription, redemption, and net asset value processes.

Asset Registry

The asset registry is the system of record for tokenized asset metadata. It connects the on-chain token to off-chain legal, financial, and operational data. This may include asset identifiers, issuer details, jurisdiction, investor restrictions, lifecycle status, and links to supporting documents.

The registry is critical because most real-world assets cannot be fully described on-chain. A token may represent a right, claim, or participation in an asset, but the legal and operational meaning still depends on external records and agreements.

Smart Contract Templates

Smart contract templates define reusable issuance, transfer, lifecycle, and control logic. Institutions should avoid one-off contract development for every asset unless there is a strong reason. Reusable templates reduce delivery risk, improve auditability, and make compliance review easier.

Templates should be designed around the asset class. A tokenized treasury, private credit pool, fund unit, and warehouse receipt may share infrastructure but require different lifecycle events, transfer restrictions, and reporting outputs.

Whitelist and Identity Registry

Tokenized assets are rarely open to every wallet on a public network. Most institutional assets require identity-linked permissioning. A whitelist or identity registry connects KYC, KYB, investor categorization, jurisdiction, accreditation, and wallet ownership to transfer eligibility.

This layer answers a simple but essential question before every action: is this wallet allowed to hold or receive this asset?

Compliance and Policy Engine

The compliance engine enforces rules before and after transfers. These rules can include jurisdiction restrictions, holding limits, blocked counterparties, investor eligibility, market conduct requirements, sanctions checks, Travel Rule data handling, and transaction monitoring.

The strongest systems do not treat compliance as a manual afterthought. They encode policy into the transaction path so that restricted transfers fail before execution and suspicious activity is surfaced with the right context for compliance teams.

Custody and Signing Controls

Tokenized assets require institutional custody. That means secure key management, wallet segregation, approval policies, transaction limits, role separation, tamper-resistant logs, and integration with risk workflows.

For banks, custody is not only the place where keys are stored. It is the control layer for who can initiate, approve, sign, and settle digital asset activity. A tokenization engine should integrate with MPC, HSM, or hybrid custody models depending on the asset value, liquidity needs, and regulatory posture.

Oracles and External Data

Many tokenized assets depend on external data: benchmark rates, prices, net asset values, collateral information, proof of reserves, corporate actions, or event triggers. Oracle integrations bring that data into the tokenization workflow.

Oracle design should be conservative. Institutions need clear data provenance, fallback procedures, exception handling, and controls around who can update or approve off-chain inputs.

Integration APIs

A tokenization engine has to connect with core banking, treasury, payments, compliance, custody, fund administration, investor onboarding, and reporting systems. The API layer is what keeps tokenized workflows from becoming a separate silo.

This is often where custom engineering creates the most value. A vendor platform may provide issuance and compliance features, but every institution has its own operating model, approvals, books and records, reconciliation process, and reporting requirements.

Which Assets Are Best Suited for Tokenization?

Not every asset class should be the first candidate for tokenization. The best early use cases are assets where the institution can define the legal wrapper, control investor access, and measure operational benefit.

Cash and Money Market Instruments

Tokenized deposits, treasuries, and money market funds are attractive because they can support 24/7 settlement, intraday liquidity, collateral mobility, and programmable treasury operations. These instruments also sit close to bank balance sheets and capital markets workflows, making them natural candidates for controlled pilots.

Fixed Income

Government bonds, corporate bonds, and structured notes can benefit from automated coupon processing, faster settlement, improved distribution, and clearer ownership records. The implementation challenge is not only issuance; it is servicing, secondary transfer rules, custody, and investor reporting over the full instrument lifecycle.

Credit and Financing

Private credit pools, securitized loans, trade finance receivables, and similar assets can use tokenization to improve transparency, investor access, and asset-level reporting. These structures require careful links between on-chain ownership and off-chain borrower, collateral, legal, and servicing records.

Real and Alternative Assets

Real estate interests, alternative fund units, commodities, and warehouse receipts may benefit from fractional ownership, transfer controls, and improved provenance. These assets also tend to have jurisdiction-specific restrictions, so identity and whitelist controls are especially important.

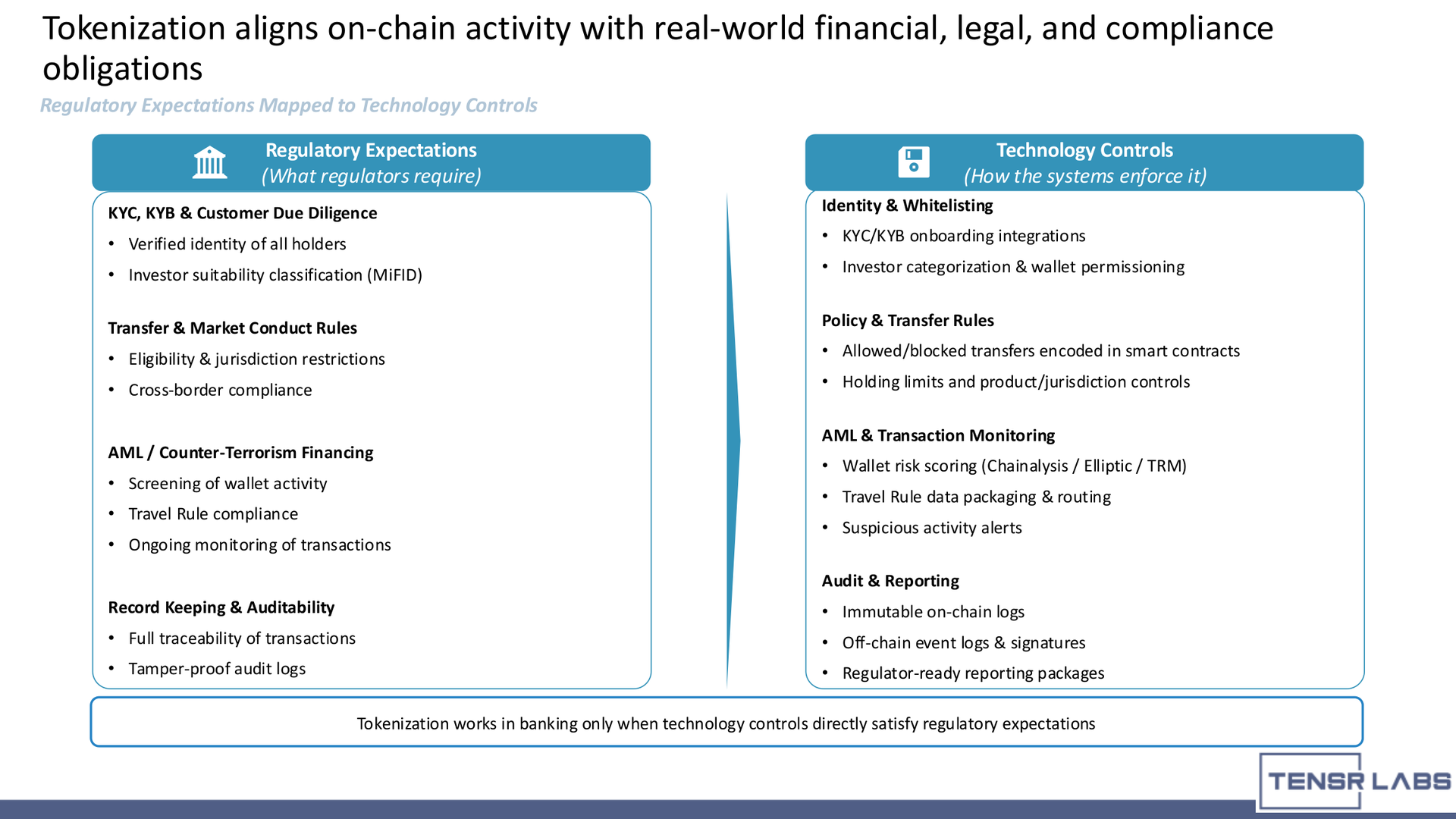

Compliance, Whitelisting, and Investor Eligibility Controls

Tokenization works in banking only when technology controls directly satisfy regulatory expectations. The core compliance challenge is to connect identity, asset eligibility, wallet permissions, transaction monitoring, and audit records into one enforceable workflow.

A practical control model includes:

- KYC/KYB onboarding for all issuers, investors, and relevant counterparties.

- Wallet ownership verification and mapping to approved entities.

- Investor classification and jurisdiction rules.

- Asset-level transfer policies enforced before execution.

- Wallet screening and transaction monitoring.

- Travel Rule data packaging where required.

- Immutable on-chain records combined with off-chain event logs and approvals.

- Regulator-ready reporting packages that explain both the transaction and the control decision behind it.

This is where tokenization engines need to work closely with custody and compliance infrastructure. The system must know not only that a token moved, but whether it was allowed to move, who approved it, which policy was applied, and what evidence supports the decision.

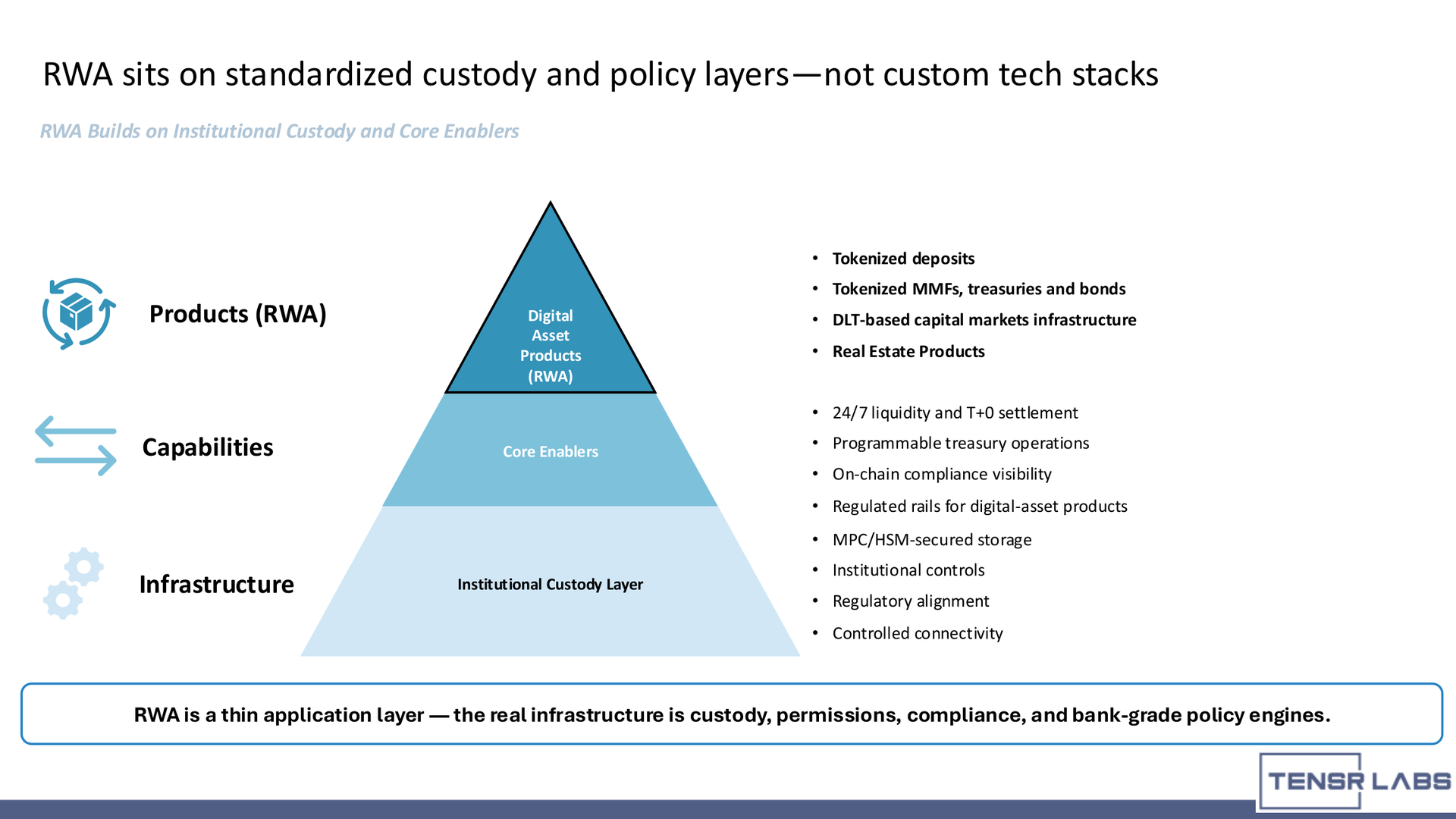

Custody, Settlement, Oracles, and Lifecycle Management

Real-world asset tokenization is a thin application layer on top of deeper infrastructure. The durable foundation is custody, permissions, compliance, settlement, and bank-grade policy enforcement.

Lifecycle management is especially important because financial assets do not stop at issuance. Bonds pay coupons and mature. Funds process subscriptions and redemptions. Credit pools produce servicing events. Deposits may be minted, transferred, and burned. Each event must be represented correctly across the on-chain token, off-chain records, accounting systems, custody controls, and investor communications.

Settlement design also matters. Some tokenized assets may settle against tokenized deposits, stablecoins, or private DLT cash legs. Others may require traditional payment rails. A robust tokenization engine should not assume a single settlement model. It should support controlled integration with the rails appropriate for the asset, jurisdiction, and counterparties.

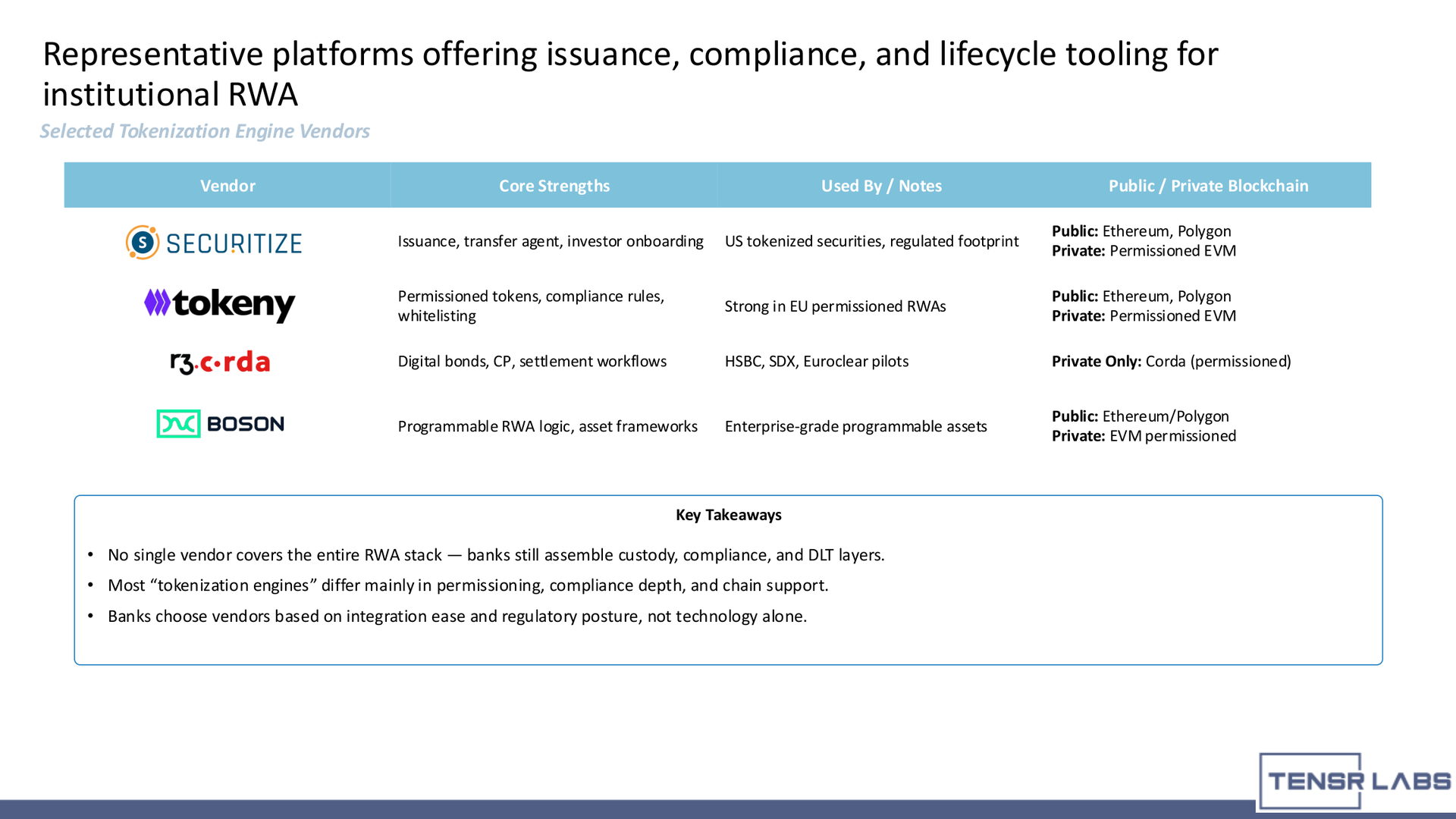

Vendor Landscape: Platforms vs Custom Integration

There are several platforms that offer issuance, compliance, and lifecycle tooling for institutional tokenization. They differ in permissioning depth, supported chains, asset-class coverage, compliance workflows, and deployment model. Some emphasize public-chain issuance with compliance modules. Others focus on private or permissioned infrastructure for regulated financial institutions.

The useful way to evaluate these platforms is through the full RWA lifecycle: origination, legal structuring, issuance, compliance, custody, settlement, distribution, servicing, reporting, and redemption. This lifecycle view is consistent with how industry frameworks describe tokenized funds and fixed income products: tokenization is not a mint event; it is an ongoing operating model.

The important takeaway is that no single vendor removes the need for institutional integration. Banks and asset managers still need to assemble custody, compliance, identity, settlement, reporting, and core-system connectivity. Vendor selection should therefore be based on:

- Asset classes in scope.

- Public, private, or hybrid chain requirements.

- Compliance and permissioning depth.

- Custody model and signing controls.

- Integration complexity.

- Regulatory posture in target jurisdictions.

- Ability to support lifecycle events, not just issuance.

For many institutions, the best path is not to build everything from scratch or buy a closed platform and hope it fits. The better approach is to define the target operating model, choose the right components, and integrate them into a controlled architecture.

How OQTACORE Can Help Build and Integrate a Tokenization Engine

OQTACORE can support institutions at three levels of maturity.

First, teams can start with a focused RWA pilot. This might involve a tokenized deposit workflow, a money market fund, a private credit pool, or a limited fixed-income issuance. The goal is to validate regulatory fit, lifecycle logic, custody model, and integration flows on a controlled scope.

Second, institutions can build reusable tokenization modules. These include issuance workflows, investor whitelisting, transfer policies, reporting exports, custody integration, and lifecycle automation aligned with internal compliance processes.

Third, OQTACORE can help design the orchestration layer that connects custody, identity, compliance engines, smart contract workflows, audit data, and core systems across public or private DLT environments.

If your team is planning a tokenized asset pilot or evaluating how tokenization would fit into existing banking, custody, or capital markets systems, OQTACORE can help map the architecture before implementation begins.

CTA: Book an RWA tokenization architecture review with OQTACORE.

Presentation diagrams

The diagrams below are adapted from the source presentation and show the architecture, controls, and vendor landscape behind the article.

FAQ

What is a tokenization engine?

A tokenization engine is the platform layer that helps institutions issue, manage, transfer, service, and redeem digital tokens representing real-world assets. It usually combines issuance tools, smart contracts, identity controls, compliance rules, custody integrations, lifecycle management, and reporting.

How is a tokenization engine different from a smart contract?

A smart contract executes on-chain logic. A tokenization engine coordinates the broader operating model around that logic, including investor eligibility, asset data, approvals, custody, off-chain records, lifecycle events, settlement, monitoring, and audit evidence.

Which assets are best suited for tokenization?

Early institutional use cases often include tokenized deposits, treasuries, money market funds, bonds, private credit, trade finance receivables, fund units, real estate interests, and other assets with clear ownership records and lifecycle events.

Why does custody matter for tokenized assets?

Custody controls who can initiate, approve, sign, hold, transfer, and redeem tokenized assets. For regulated institutions, custody is not only key storage; it is a governance and operational control layer.

Do banks need a private blockchain for tokenization?

Not always. Some tokenized assets can use public networks with strong compliance and custody controls. Others require private or permissioned DLT because of privacy, governance, settlement, or regulatory requirements. The right model depends on the asset, counterparties, jurisdiction, and operating model.

References

- RWA.xyz, Tokenized U.S. Treasuries

- CoinDesk, BlackRock's BUIDL becomes largest tokenized treasury fund

- Franklin Templeton, Franklin OnChain U.S. Government Money Fund

- ESMA, DLT Pilot Regime

- Monetary Authority of Singapore, Project Guardian